The Debasement Decade

Seven Assets Against True Inflation — and What You’re Actually Trusting

A 10-year cross-asset study · as of June 18–20, 2026

Introduction

This report examines seven assets — NVIDIA, the Nasdaq-100, the S&P 500, gold, silver, Bitcoin, and the 10-year US Treasury — through two lenses over a ten-year horizon. The first is return measured against a realistic cost of living rather than the official inflation print. The second is the counterparty risk you accept to hold each asset. The two are usually studied apart; held together, they tell one story.1

The past decade has a clear shape. NVIDIA (first through gaming and more recently from AI) dominated everything, compounding at rates normally reserved for venture portfolios. Gold and silver staged a genuine resurgence, ending a sleepy 2010s. The S&P 500 and Nasdaq-100 posted unusually high returns for broad indices — propelled by the same AI names and by the first wave of monetary debasement that ran from the 2020 stimulus through 2026. Bitcoin produced the highest ten-year number of all, but in bursts: stripped of its early years, its recent performance has lagged every other asset on this list, leaving it today in a deep drawdown. That is the trailing picture — scarcity and silicon, with Bitcoin’s engine idling.

The forward picture inverts it, and that inversion is the report’s central claim. The assets that won the last decade did so largely by re-rating to rich valuations, and a valuation cannot re-rate from a record twice; the math that produced their past returns now works against them. Once returns are measured against true inflation rather than the official figure, the inversion deepens into something stranger: the “safe” asset — the Treasury — becomes the surest way to lose purchasing power, while the volatile, out-of-favor asset bought in a drawdown carries the best odds of preserving it. The unifying force underneath is debasement, and the sections below trace it from where it has been to where it leads.

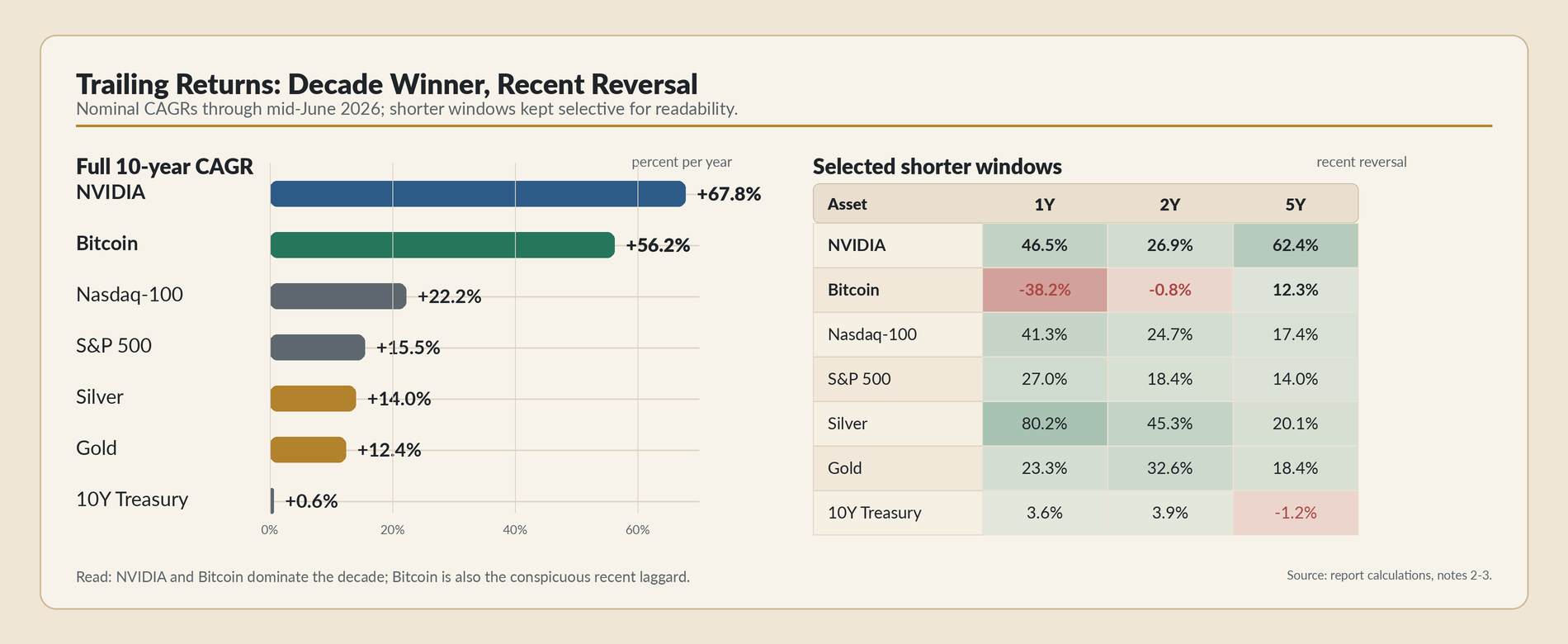

1. The Trailing Decade

Nominal CAGRs through mid-June 2026, with the full-decade result separated from selected shorter windows for readability:23

The story reads cleanly across the rows. NVIDIA’s two-thirds-per-year decade reflects a company that first rode gaming and GPU compute, then the post-2022 AI boom. The Nasdaq and S&P, at 22% and 15.5%, are extraordinary for broad indices — a product of the same handful of AI winners and of the asset-price inflation that easy money produced after 2020. Gold and silver, dead money for much of the prior decade, compounded in the teens as central banks accumulated and real yields stayed suppressed. And Bitcoin, whose 56% leads the ten-year column, tells the opposite story at the short end: negative over one and two years, it has been the worst-performing asset on the list recently, measured down from the ~$125k highs of mid-2025 into today’s drawdown. The same asset is the decade’s champion and the past two years’ laggard, depending entirely on where the clock starts — a fact that becomes the hinge of the forward analysis.

2. The Real Inflation Rate

Most people do not experience inflation as a broad statistical basket. They experience it through five expenses that dominate a household budget: housing, vehicles, groceries, health care, and education. These are the line items that set the felt rate — the one that governs how secure a family feels and how it votes. Of the five, two have genuinely improved. A 2026 car is safer and a 2026 course of cancer treatment is more effective than their 1990 equivalents, and the official statisticians are right to credit that quality. But housing, groceries, and education have simply grown more expensive, with no comparable leap in what you get.

The trouble with crediting the improvements in the other two is that they are essential, and the improvement is often unaffordable. Better health care you cannot pay for does not register as progress; it registers as exclusion — you feel like a failure for not having the better thing, not grateful that it exists somewhere. A car loaded with safety technology and a price tag you must finance over seven years is not self-evidently a gain for the household holding the note. Economics is a human discipline, and the inflation rate that actually shapes behavior is the rate on the things you cannot opt out of. Measured against those essentials, and against broad-money growth of 6–7% in normal years and far more after 2020, lived inflation has run well into the double digits. The official methodology, by contrast, has been revised only ever downward since 1980 — through substitution adjustments, hedonic credits, and a survey-based proxy for housing — against a clear institutional incentive to under-report.4 We therefore use CPI + 7 (similar to the 1980 unadjusted CPI methodology) not as a forecast but as a deliberately stringent bar: anything that clears it has unambiguously grown real purchasing power.5

Applying that bar to the decade just past already reframes it. The S&P’s celebrated 15.5% becomes roughly +5% real; gold and silver shrink to low-single-digit real returns that mark them as hedges rather than engines; and the 10-year Treasury, the textbook safe asset, reveals itself as a machine that destroyed about −9% of purchasing power per year. The forward question is which assets can clear the same bar going the other way.

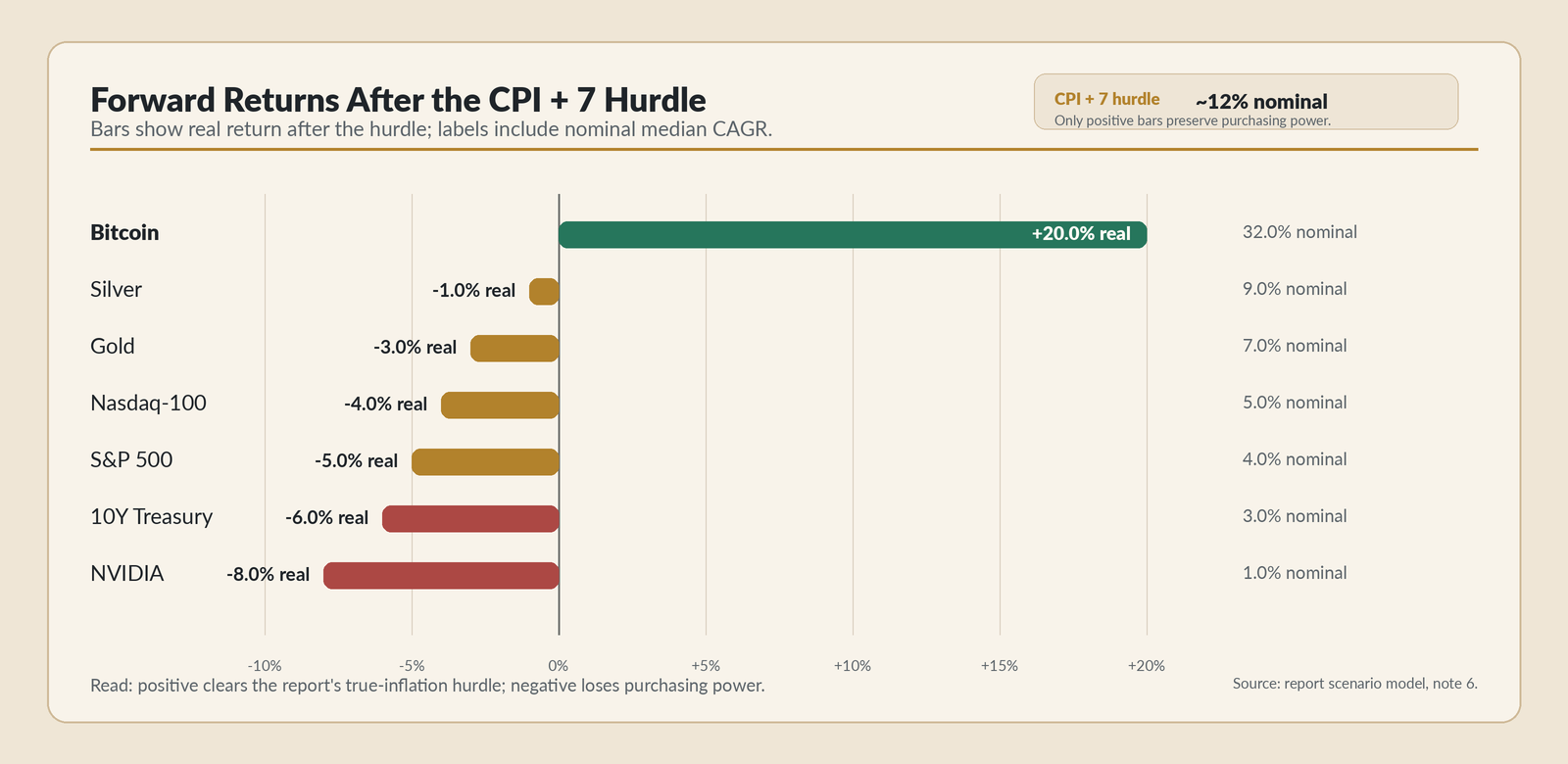

3. The Forward Decade — Base Case

The base case assumes orderly fiat debasement — the muddle-through path, neither an AI miracle that repairs the public balance sheet nor an outright collapse. Within it, each asset’s central (median) ten-year outcome looks like this:

The shape of this figure is the whole argument. Only Bitcoin clears the hurdle with room to spare. The metals roughly tread water in real terms. The broad equity indices and NVIDIA lose ground in real terms even as their nominal prices likely keep rising — the debasement that lifts the headline number is the same force eroding its purchasing power. And the Treasury, the conventional anchor of a “safe” portfolio, is a guaranteed real loss with a zero percent chance of clearing the bar.

Why should Bitcoin separate so far from the rest, and from a hard-money cousin like silver in particular? Because all seven assets sit in the same debasement current but capture it differently, and Bitcoin is the only one that captures it three ways at once. It is absolutely scarce, like gold, so it holds value as the currency dilutes. It is early in monetization, unlike gold, so it carries adoption and re-rating upside on top of the debasement — a second engine the metals no longer have; and unlike gold it never had to choose between storing value and being usable money, because it already settles final, bearer value across borders at the speed of information — beating gold on the very axis where gold is weakest, at a fraction of gold’s market capitalization. And it is cheap right now, bought in a 44% drawdown, so today’s entry embeds a re-rating back toward trend that a buyer at the highs would forgo. Silver shares only the first of these: it is scarce and it benefits from a real industrial deficit, but it is a hedge that has already run — fresh off an 80% year, it is expensive, and from an expensive start even a good fundamental story compounds slowly. Gold is the same logic, lower beta. The equity indices capture debasement only nominally and begin at record valuations, so their multiples can fall but not expand. Bonds have no scarcity at all and a fixed nominal claim — the pure victim. Bitcoin’s edge is not that it is the only good asset; it is that it is the only one stacking scarcity, monetization, and a cheap entry in the same position.67

That triple stack is also why Bitcoin’s distribution is the widest, and the honest way to hold it is as a fork rather than a forecast. If Bitcoin keeps making new highs across the coming cycle, the monetization thesis is intact and it compounds toward a seven-figure price. If a full cycle passes without one, the reflexivity that drives a pre-majority monetary asset runs in reverse and it washes out — but a washout (drifting to a disappointing level from which today’s distressed entry still leaves a holder roughly whole) is not the same as a wipeout (a true protocol death, which is a small and separate tail, modeled here as less likely than a full dollar hyperinflation). The branch weights and price targets behind the +32% median are detailed in the notes; the point for the body is that the central case is high, the upside tail is fat, the literal-loss tail is thin, and the whole thing is anchored to a cheap cost basis.

NVIDIA deserves a closing word as the base case’s cautionary mirror. Its +1% median with wide variance is not a typo; it is what a binary bet looks like when you average it. The bull case (a continued AI-capex super-cycle) and the bear case (a Cisco-style multiple collapse in which earnings keep rising while the stock does not) roughly cancel, leaving a distribution centered near zero — the precise opposite of the certainty its trailing 68% implies. The gap between NVIDIA’s reputation and its forward odds is the single widest in the base case.89

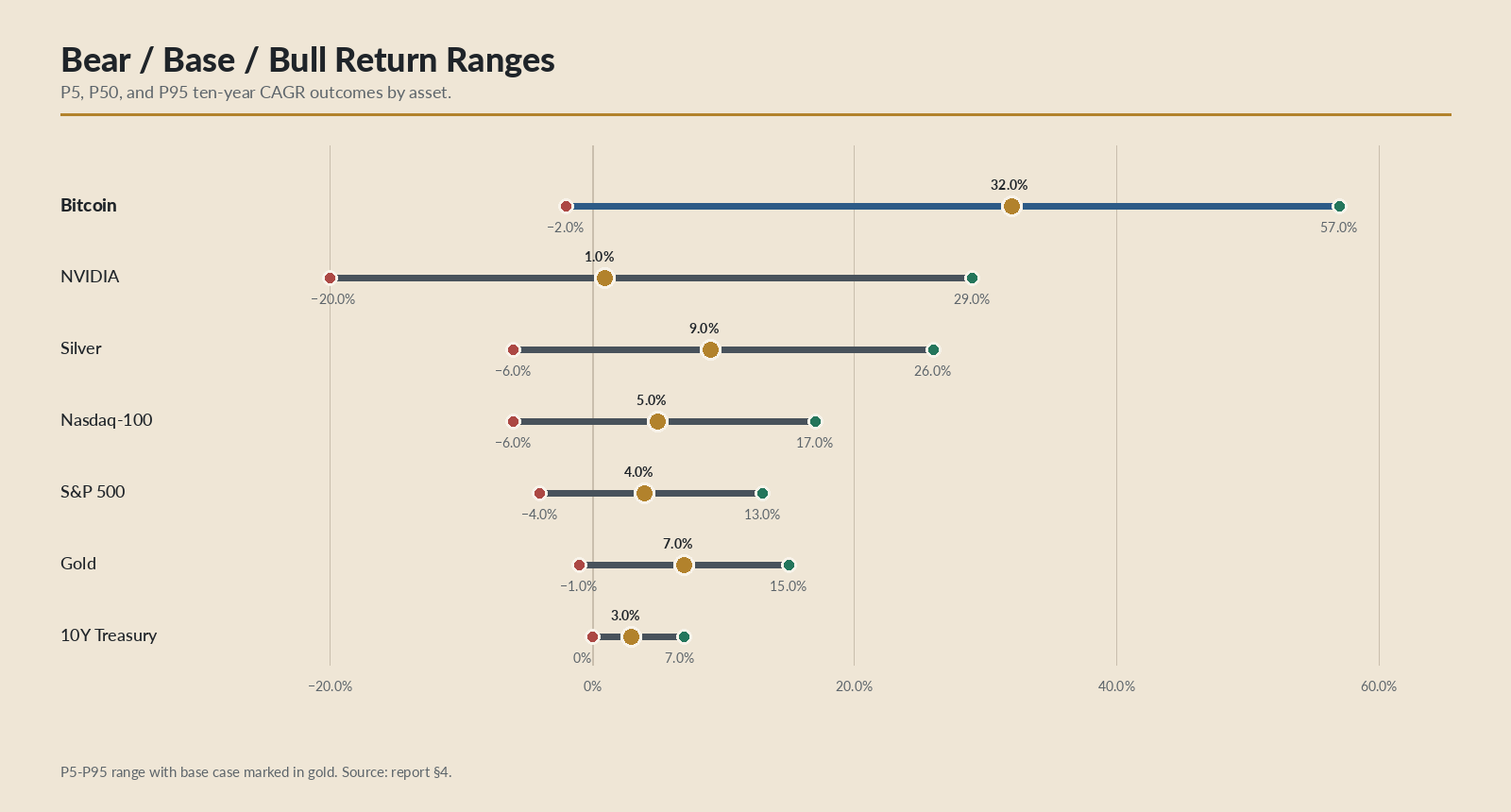

4. The Alternative Cases

The base case lives inside one regime. Its honesty depends on taking the others seriously, and the range of ten-year outcomes — the bear (5th percentile), base (median), and bull (95th percentile) of each asset’s simulated distribution — frames where the surprises hide:

Note the asymmetry: Bitcoin’s bear case (−2%) is shallower than the Nasdaq’s, while its bull case dwarfs everything — the signature of an asset bought cheap with optionality intact. Three regime shifts would push outcomes toward those tails.

An AI productivity boom would re-rate today’s “expensive” equities into cheapness against a higher growth path — but the channel that ultimately caps their returns is not laid-off workers selling stock (the bottom 90% own only ~10% of equities). It is demand destruction as the economy automates its own consumers, followed by the inevitable policy response: universal basic income funded by the printing press, which is debasement under another name and most likely arrives after a nominal melt-up. AI success, in other words, still routes through the dollar’s dilution; equities may never fall nominally, yet they decay in real terms like everything else priced in fiat.

A monetary-regime rupture is the mirror image — the same “does fiat keep its monopoly?” question answered the other way, carried in the model as a roughly 6% up-tail spanning gold remonetization through hyperinflation. It is the scenario that inverts the distribution hardest: the Treasury loses essentially all real value, gold and Bitcoin soar, equities muddle. The caveat specific to gold is that it demonetized for a reason — settlement could not keep pace with information — and that vaulted gold is as seizable as a Treasury, so its neutrality is real only if repatriated, at which point it is slow. The reserve-asset trilemma (neutral, fast, deep — pick two) leaves gold the least-bad available neutral reserve today, with the neutral-digital endgame pointing at Bitcoin.

A stall in Bitcoin’s adoption is the bear case against the report’s own conclusion. If the Power Law is merely the top half of an S-curve, a maturing Bitcoin becomes a 5%-return NASDAQ proxy, and the evidence usually offered is on-chain: daily active addresses near 636k, far below 2021’s 1.36 million, never reclaiming a million across a bull market. But that evidence measures the wrong layer and rests on a conflation worth dismantling. The gold-parity target that anchors the bull case is a store-of-value proposition — gold’s ~$28T is almost entirely monetary-reserve value, with essentially no payments function — so Bitcoin needs no medium-of-exchange adoption to reach it; demanding proof of payments use grades it against a thesis the target never required. And where payments use is the question, Bitcoin already wins: it settles final, bearer value across borders at the speed of information, which gold cannot, and that activity has migrated to second layers the base-chain metrics cannot see. Lightning’s routed dollar volume crossed $1 billion per month in late 2025 — roughly 400% growth in the year, at a 99.7% settlement success rate — even as public channel capacity, like the UTXO set, plateaued; Strike alone processed over $6 billion in 2024, Tether’s USDT now settles over Lightning via Taproot Assets (reaching its 350M+ users), and bridges such as Kenya’s Tando have made tens of millions of mobile-money accounts Lightning-addressable.10 Active addresses are flat because the network grew up into layers, not across the base chain. The honest residual bear case is therefore not “Bitcoin isn’t used,” but “does it keep taking store-of-value share from gold and bonds” — a question the holder and network fundamentals in §7 answer, not the active-address count. Which regime you weight most heavily is, ultimately, the investment decision, and §7 argues it should be made on fundamentals rather than price.

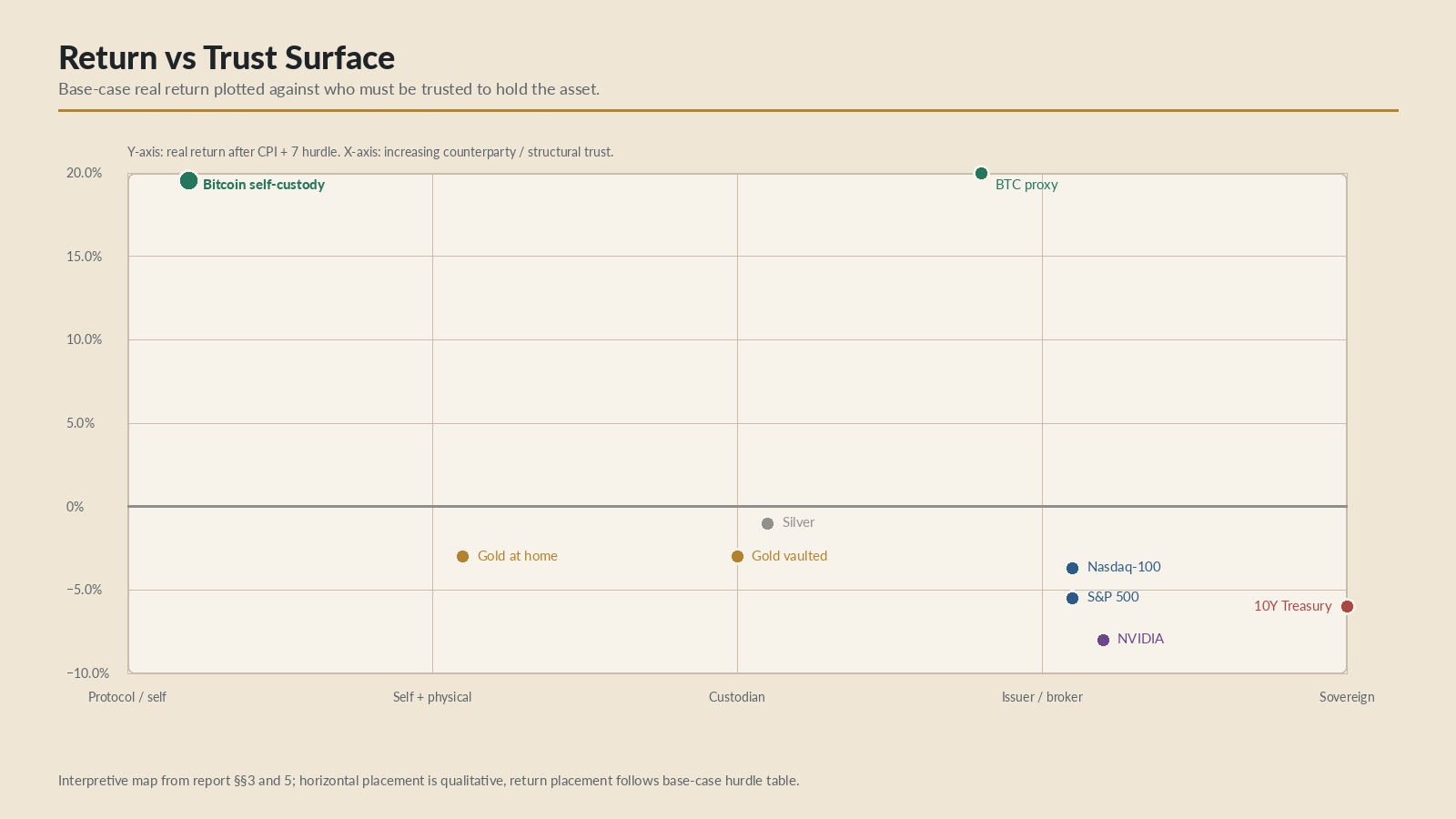

5. What You’re Actually Trusting

The return analysis answers which asset pays. The harder question is what you are trusting to collect, and whether you can see and bear the risk. Owning a 10-year Treasury is lending to the US government; that trade paid off for generations because the trust was honored. The mistake was never trusting the sovereign — it was forgetting the trust was being extended at all, and ceasing to price it. The same discipline applies to every line below.

There is no trust-free option, but there is a clear hierarchy, and monetary history points to a winner rather than a draw: when sound and debasing money compete, Gresham’s law drives the bad money into circulation and the good into savings, and over a long enough horizon the harder money takes the store-of-value role outright. The asymmetry the map most understates is custody itself: of these seven, Bitcoin in self-custody is the only one you can actually hold — a bearer asset with no counterparty. Gold at home is the next closest, with the physical frictions noted. Everything else is an irreducibly custodial claim — a Treasury or a corporate bond is a ledger entry at an institution, and you can no longer even take possession of a stock certificate, since US shares are held in street name, almost all of them ultimately registered to Cede & Co., the DTCC’s nominee, which leaves you the beneficial owner of a claim rather than the owner of the thing. ETF wrappers merely stack another intermediary onto an asset engineered to need none.

Self-custody does carry real operational risk: keys are lost, mistakes have no undo, and that risk must be respected by anyone who takes it on. But it is the wrong risk to fear most, because the historical base rate is nearly one-sided — states and institutions have confiscated, frozen, defaulted on, and above all inflated away vastly more wealth than individuals have ever lost to their own carelessness, and even the best-run governments do it quietly through the currency (the Treasury’s −9% real is the receipt). The operational risk of self-custody is at least yours to control; the counterparty risk of everything else is not yours at all. For anyone willing to learn the discipline, trusting yourself over the institution is not naïveté — it is the empirically safer side of the trade, and Bitcoin is the only asset here that even offers it.

6. Time, Not Timing

The edge in everything above is structural and slow: it is paid out over a decade of debasement and monetization, and it is collected by holding through volatility, not by trading it. That distinction is the line between the strategy’s return and its ruin, because the measured record of active trading — retail and, as far as the thin data reach, professional alike — is close to uniform failure, and the very volatility that makes a monetizing asset a superb hold is what lures traders to their destruction.11 A large share of “Bitcoin skeptics” are simply people who tried to trade it, were chopped up by that volatility, and blamed the asset for a loss their method made near-certain. The hardest thing this report asks is therefore also the simplest: once you own the right things, do nothing — on purpose.

7. Conclusions and a Fundamentals Watch-List

Bitcoin is by far the best forward return against a true-inflation hurdle here — roughly an 81% chance to clear it, a +20% median real return — and the reflexive “but it’s so risky” that greets that result is largely the voice of the incumbents the asset threatens: the banks it disintermediates, the central banks whose monopoly on issuance it ends, the entrenched and the corrupt who depend on an opaque and captured financial system, and governments that rule through control of the financial rails. To them, Bitcoin is genuinely dangerous. To a self-custodial individual it is closer to the opposite — an exit from exactly those parties. The risks that actually fall on the holder are narrower and more honest: that it fails to keep monetizing and washes out (the model uncertainty quantified above), and that self-custody demands a discipline not everyone will learn. Volatility is not a defect but the price of monetizing in real time, and it compresses as the asset matures; regulatory hostility is not a warning label but the predictable reflex of the system being routed around. The holder’s real question is the one this report’s fundamentals track — does Bitcoin keep taking monetary share — not the borrowed anxiety of the institutions it disrupts.

The other assets are different trades, each priced for what it trusts: bonds a near-certain real loss for a nominal guarantee, equities a nominal melt-up that decays in real terms, NVIDIA a binary AI bet, the metals a bounded hedge. The failure common to all of them is the same — holding a trust position without remembering you hold it.

The report is ultimately a method for using fundamentals to make investment decisions, and that is the spirit of the watch-list below. Price is a lagging, noisy verdict; it neither confirms nor refutes a thesis on any useful timeline. The signals worth tracking are the underlying drivers, because they move first and they move for reasons:

- Bitcoin monetization (the core thesis). Is the self-custodying share of supply rising? Are realized capitalization and non-zero-balance addresses making higher highs each cycle? Is the holder base broadening and coins continuing to leave exchanges? Are more sovereigns following Iran into settlement use, and are institutions accumulating rather than renting through ETFs? These confirm or deny monetization before price does.

- The pace of debasement. Broad-money (M2) growth, the federal deficit and debt trajectory, real yields, and any drift toward yield-curve control or financial repression. These set the tailwind for every scarce asset and the headwind for every fiat claim.

- AI’s return on capital. Not NVIDIA’s stock, but whether the ~$700B/yr of hyperscaler capex begins to show measurable enterprise returns — the fact that would validate the equity bull case — or whether guidance is cut, which would trigger the bear.

- Second-layer throughput — the medium-of-exchange axis gold cannot contest. Lightning’s routed dollar volume and settlement-success rate, stablecoin settlement over Taproot Assets, and fiat/mobile-money bridges (Strike, Kenya’s Tando, Machankura) — the usage that base-chain metrics structurally miss, and the clearest live evidence that Bitcoin’s money-ness is deepening even while on-chain activity looks flat.

- The official-sector bid for hard money. Central-bank gold tonnage and the structural silver deficit (solar demand against byproduct-constrained supply) — the fundamentals beneath the metals’ role as hedges.12

The position logic that falls out of this is not advice, but it is the logic of the analysis: size exposure to the scarce, debasement-resistant asset with the best forward risk/return, and decide consciously how much to hold in self-custody versus a proxy. Hold the metals as a bounded hedge, treat equities as nominal-up and real-down, and avoid duration. Above all, keep every position’s trust assumption explicit and re-priced — because the debasement decade rewards the assets that need no one’s permission and punishes the ones whose risks their owners have stopped watching.